Living Benefits Life Insurance in the U.S. – Get Paid While You’re Alive

Angela was only 42 when Stage III cancer hit. The shock was immense, not just personally, but financially. Medical bills and the fear of not providing for her family were terrifying. Luckily, Angela had living benefits life insurance. It became her financial lifeline, allowing her to access cash early from her policy. This meant she could focus on getting better, free from crushing money worries. Her living benefits life insurance kept her afloat when life threw a curveball, proving it’s for living, not just for after you’re gone.

In the U.S., where healthcare costs can be absolutely bonkers and a surprise illness can wreck even the best-laid plans, living benefits life insurance is a game-changer. This isn’t some dusty old policy; it’s a modern, powerful financial tool that protects your loved ones after you’re gone, and more importantly, protects you and your family when serious health stuff pops up.

Table of Contents

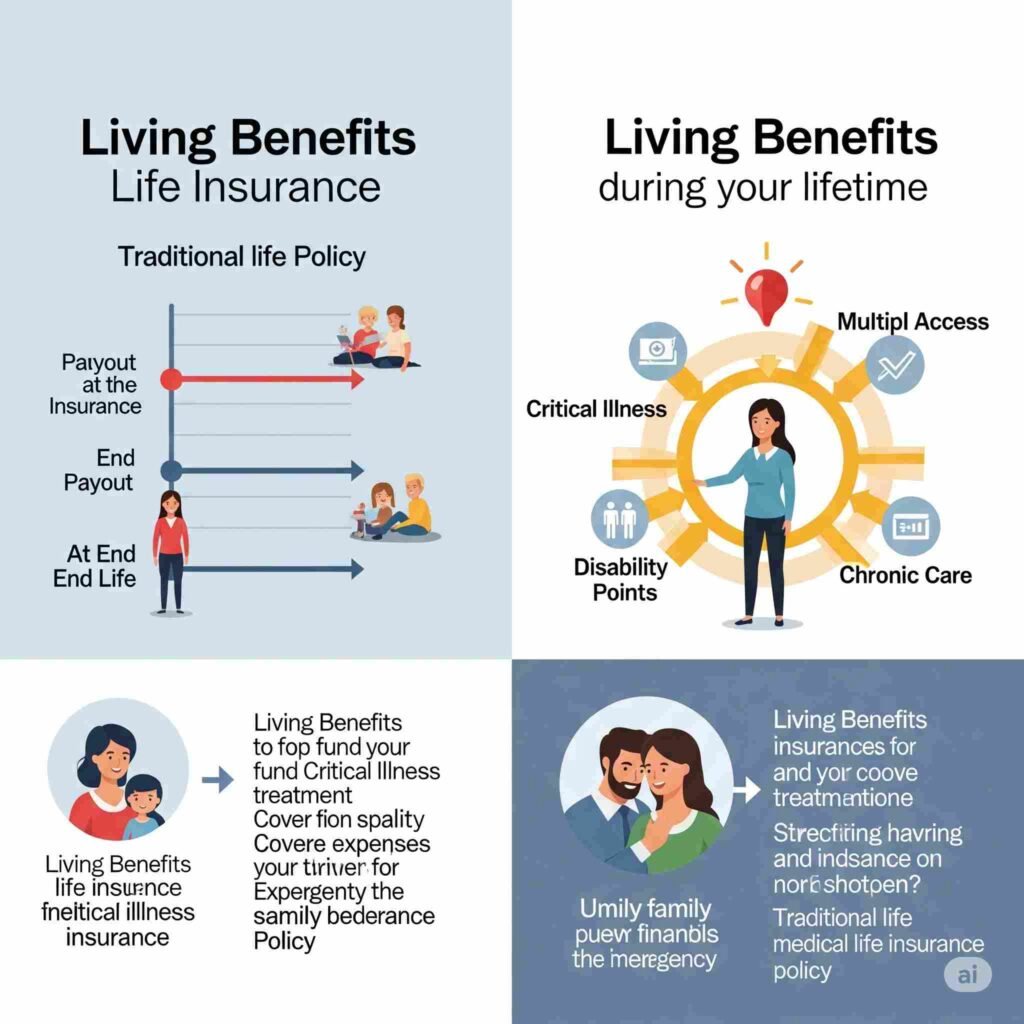

So, What’s Living Benefits Life Insurance Anyway?

Alright, let’s break it down. Living benefits life insurance is basically a life insurance policy that lets you tap into some of your payout before you pass away, under specific tough health situations. We’re talking stuff like a terminal illness, a chronic illness, or a critical illness. Regular life insurance only pays out when you die. But living benefits life insurance hooks you up with cash when you need it most – during your lifetime. That means you can use the money for medical bills, fixing up your house, covering lost paychecks, or just keeping your everyday life going.

These “living benefits” are usually add-ons or built right into permanent life insurance policies (like whole life or universal life) and sometimes even term life policies. You’ll hear them called things like:

- Accelerated Death Benefit (ADB) Riders: This is the most common one. It lets you get a chunk of your death benefit if doctors say you’ve got a terminal illness and maybe 12 or 24 months left (depends on the company).

- Critical Illness Riders: These pay out if you get diagnosed with a serious critical illness like a heart attack, stroke, cancer, or kidney failure. What’s covered can be different from policy to policy.

- Chronic Illness Riders: This one kicks in if you can’t do a few basic daily things on your own – like bathing or dressing – or if you have serious memory problems. It can help cover long-term care costs.

- Long-Term Care (LTC) Riders: Similar to chronic illness riders, but these are specifically for paying for long-term care, whether you need help at home, in an assisted living place, or a nursing home. https://primelifecover.com/cancer-survivor-life-insurance-options-2025/

The cool thing about living benefits life insurance is how flexible it is. It gets that life doesn’t always go to plan, and that money stress during a health crisis can be just as brutal as the illness itself. For Americans dealing with crazy healthcare costs and the emotional toll of getting sick, living benefits life insurance offers a crucial extra layer of protection.

Who Needs This, and Why?

If you’re between 30 and 60, living in the U.S., and you’re sweating about how a future illness could mess with your finances, then living benefits life insurance should be on your radar. Here’s why:

- Family Health History: If serious illnesses like cancer or heart disease run in your family, this policy can give you peace of mind, knowing you’ve got a cash cushion if something similar happens to you.

- Worry About High Medical Bills: Even with health insurance, those out-of-pocket costs, deductibles, and co-pays can add up fast. Living benefits life insurance can help fill that gap.

- You’ve Got Folks Relying on You: If you’ve got a spouse, kids, or anyone else who counts on your paycheck, getting sick and not being able to work can be a disaster. Living benefits can help replace that lost income.

- Business Owners: If you own a business, getting sick can bring everything to a screeching halt. Living benefits can provide cash to keep the business going or cover your personal bills while you recover.

- Thinking About Long-Term Care: Long-term care in the U.S. costs an arm and a leg. A chronic illness rider in your living benefits life insurance can seriously lighten that load, keeping your savings safe.

- Smart Planners: If you’re someone who plans ahead and knows that dodging financial risks is key, then living benefits life insurance is a powerful tool to have in your corner.

Basically, anyone who gets that an unexpected health crisis can torpedo their financial future should check out living benefits life insurance. It’s all about protecting your money, your family, and your peace of mind while you’re still kicking.

Living Benefits vs. Old-School Life Insurance

The big difference between living benefits life insurance and regular old life insurance is when you get the money.

| What It Is | Regular Life Insurance | Living Benefits Life Insurance |

| When It Pays | When the insured person dies | When the insured person dies OR if they get a serious illness |

| Why You Get It | Money for your family after you’re gone | Money for your family after you’re gone AND for you if you get sick |

| Can You Get Cash Early? | Nope, only after death | Yep, you can get some of the death benefit while you’re alive |

| Main Focus | What happens after you’re gone | What happens if you get sick, and after you’re gone |

| Cost | Usually cheaper (especially for term) | Can be a bit more expensive because of the extra perks |

| How Flexible Is It? | Not much flexibility in getting money early | Super flexible – use the cash for whatever you need (medical, bills, etc.) |

While regular life insurance is super important for taking care of your loved ones down the road, it doesn’t do squat for the money problems that hit before you die because of a bad illness. Living benefits life insurance fills that gap, turning a payout that was just for after you’re gone into something you can use while you’re still here. This is a huge deal with how healthcare is set up in the U.S., where being sick can be just as financially crushing as it is physically. A lot of Americans are realizing that a policy that only pays out at death just isn’t enough these days. Adding living benefits life insurance truly completes your financial safety net.

How to Get Living Benefits Life Insurance in 2025

Getting living benefits life insurance in 2025 is pretty much like getting regular life insurance, but you’ll want to pay extra attention to those living benefit add-ons. usa.gov

- Figure Out What You Need: How much coverage do you really need? Which living benefits are most important to you (like critical illness, chronic illness, terminal illness)? Think about your age, health, bills, and if there’s any sickness in your family history.

- Shop Around: Not every insurance company offers the same awesome living benefits. Look for companies with good reputations and strong financial ratings. Some names to check out are Transamerica, Protective, National Life Group, and Pacific Life – they’re known for good living benefit options.

- Talk to a Pro: This is key. A sharp life insurance specialist can help you sort through all the different policies, explain how each living benefit works, and help you compare prices. They’ll also make sure you understand when you can get a payout and if there are any catches.

- Fill Out the Paperwork: You’ll give them your personal info, money details, and health history. Be honest and thorough.

- Medical Check-Up (Maybe): The insurance company will review your application, medical records, and might even ask you to do a quick medical exam. They’re checking you out to figure out your risk and how much your premiums will be.

- Read the Fine Print: Once you’re approved, read that policy document carefully. Pay close attention to the details of the living benefits life insurance riders – like what specific events trigger a payout, how much you can get, and if there are any waiting periods.

- Activate and Pay: Once you say yes to the policy and make your first payment, your living benefits life insurance coverage kicks in.

Remember, getting living benefits life insurance is a smart move for your future and your peace of mind. Taking the time to understand your choices and working with an expert will make sure you get the right coverage for you. https://primelifecover.com/ai-life-insurance-usa-2025/

Top Perks of Living Benefits Life Insurance

| What You Get | What It Means for You |

| Financial Lifeline | Gives you a financial cushion during health emergencies, so you don’t go broke from medical bills or lost paychecks. This is the main reason to get living benefits life insurance. |

| Cash You Can Use for Anything | Unlike health insurance, the money you get from living benefits can be used for whatever you need – medical stuff, house payments, utility bills, trying new treatments, remodeling your home, or just keeping your life comfortable. |

| Protects Your Savings | Stops you from draining your savings, investments, and retirement funds to cover unexpected medical or long-term care costs. This feature alone makes living benefits life insurance super valuable. |

| Chill Out | Knowing you have financial backup for the unknown lets you focus on getting better instead of freaking out about money. The emotional relief from living benefits life insurance is huge. |

| Tax Smart | Most of the time, the early payouts from living benefits life insurance are tax-free under current U.S. tax laws, just like a death benefit. (Always check with a tax pro for your specific situation.) |

| All-Around Coverage | It combines regular life insurance with critical illness, chronic illness, and terminal illness coverage, giving you one beefy financial protection plan. This makes living benefits life insurance a killer solution for modern financial planning. |

| Keeps Up with Costs | Some policies actually increase the payout amounts over time to keep up with rising costs of living and healthcare, making your living benefits life insurance even more valuable down the road. |

Life’s a wild ride, and while we can’t always control the curveballs, we can get ready for them. Living benefits life insurance changes the game – it’s not just for when you’re gone, it’s a smart asset that protects your money and well-being through thick and thin. For Americans between 30 and 60, especially if you know how financially crushing a serious illness can be, checking out living benefits life insurance isn’t just a good idea, it’s a must.

Q:1 Is living benefits life insurance worth it?

A: Yes, for financial protection during health crises in the U.S.

Q:2Can I get a payout before death?

A: Yes, for qualifying illnesses (terminal, critical, chronic).

Q:3 Is it more expensive than term life?

A: Generally yes, due to added lifetime benefits.

Q:4 How’s it different from critical illness cover?

A: Critical illness is a type of living benefit; policies may include more.

Q:5 What can I use the early payout for?

A: Anything: medical bills, living expenses, lost income, etc.

✅ Disclaimer:

This article is just for general info. For personalized insurance advice, talk to a certified expert.

Call To Action

“Ready to protect your family’s future? Compare the best life insurance plans today and make the right choice with confidence.”

📢 Stay connected for the latest insurance tips, updates, and guides!

👉 Follow us on Facebook

👤 Author Box: Written by DN Patel Founder & Life Insurance Specialist Helping families in USA, UK, Canada & Australia choose the right life cover.

One Comment