UK Life Insurance Suicide Clause Explained: When Does It Pay Out? (2025 Guide)

The phone rang just after the school run, and Sarah’s heart sank. It was the insurance company. Her husband, Mark, a man who loved his family more than anything, had died just three months earlier. He had always been so practical, so organised. He’d taken out a life insurance policy, a big one, telling her, “This will look after you and the kids, no matter what.”

But a few weeks ago, a nagging doubt had started to creep in. A neighbour mentioned a UK life insurance suicide clause. Sarah’s stomach flipped. Would the policy be void? Would her children’s future, the one Mark had worked so hard to secure, be gone just like that? The fear was overwhelming.

This is a fear that many people in the UK have, but rarely talk about. When we sort out our life insurance, we’re planning for the worst. But what about the absolute worst? This guide will get straight to the point and explain exactly what a UK life insurance suicide clause is, how it works in 2025, and when a claim will be paid out. We’ll cut through the jargon and give you the real-world facts you need to feel confident and secure.

Table of Contents

What on Earth is a UK Life Insurance Suicide Clause?

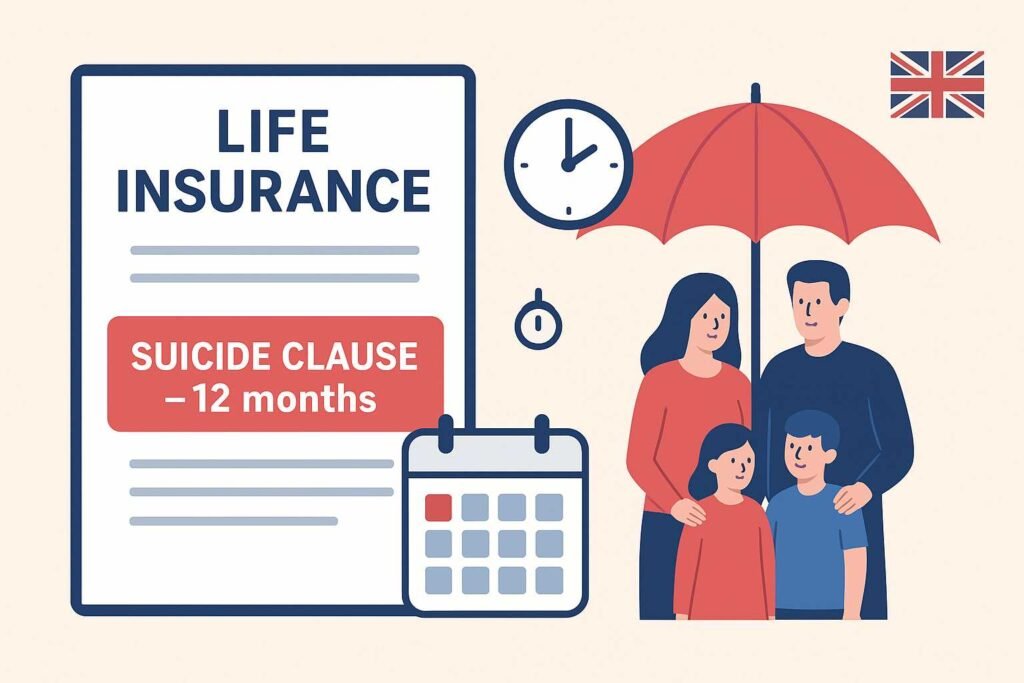

A UK life insurance suicide clause is a standard little rule tucked into pretty much every single life insurance policy. In plain English, it means that if a person dies by suicide within a certain amount of time after the policy starts, the insurance company won’t pay out the full amount.

This rule isn’t there to be mean; it’s there to stop something called ‘fraud’. Without it, someone in a desperate state could take out a massive life insurance policy with the plan to end their life, just to give their family a big lump sum of cash. This would be a massive problem for insurers, and they’d have to put everyone’s premiums through the roof to cover the risk. The UK life insurance suicide clause keeps the whole system fair and affordable for all of us. UK Financial Conduct Authority (FCA)

The time limit for this rule is called the ‘exclusion period’. For most UK policies, this is either 12 months or 24 months. The big players in the UK, like Legal & General, Aviva, and Royal London, almost all use a 12-month period. That means if a person dies by suicide more than a year after they took out the policy, their family will get the full payout, simple as that.

Don’t Mix It Up: The Exclusion Period vs. The Contestability Period

It’s easy to get confused. The UK life insurance suicide clause is part of a bigger rule called the ‘contestability period’, which also usually lasts 12 to 24 months. This is the time when the insurance company can check if you told the absolute truth on your application.

For example, if you forgot to mention a serious health issue or your smoking habit, the insurer could refuse a claim. A death by suicide during this time would also be investigated, but specifically under the rules of the UK life insurance suicide clause. After this period ends, the insurer’s ability to question the claim is much, much smaller.

The Big Question: When Will a Policy Pay Out for Suicide?

This is the key point. The answer depends completely on the timing.

Scenario 1: Death Within the First Year (or Two)

If the person dies by suicide within the first 12 or 24 months of the policy, the insurance company will not pay out the full death benefit. Instead, they will usually give back all the premiums that were paid up to that point. It’s not the huge sum of money the family was expecting, but it’s a small bit of help, and it’s an important part of the UK life insurance suicide clause that shows a little bit of compassion.

Scenario 2: Death After the First Year (or Two)

If the person dies by suicide after the UK life insurance suicide clause exclusion period is over, the life insurance policy will pay out the full amount. This is the most common situation, as most people hold their policies for a very long time. The insurer will treat the claim just as they would any other cause of death. You see, the UK life insurance suicide clause isn’t a forever denial; it’s just a temporary rule for the very start of the policy.

Sorting Out a Claim after a Suicide

Dealing with a life insurance claim after a suicide is a hard and emotional time. Knowing what to expect can take a little bit of the pressure off.

A Simple Step-by-Step Guide:

- Tell the insurer:

The person who’s going to get the money, or any close family member, should call the insurance company and inform them about the death. - Get the Documents Ready: The insurer will need a few key bits of paper:

- The original policy document.

- The death certificate, which will show the cause of death.

- The coroner’s report (if there was an inquest).

- What the insurer does:

If death happens in the first exclusion period, they check the death certificate and coroner’s report. If it’s marked as suicide, they don’t pay the claim — they just return the premiums. - Getting the Payout: If the death happened after the exclusion period, and everything else on the application was truthful, the insurer will process the claim and pay the money to the named beneficiaries.

For more details on the general claims process, you can have a look at our guide on [How to Make a Life Insurance Claim in the UK].

Mental Health and Life Insurance in 2025

The way we talk about mental health in the UK has changed a lot, and this has also changed how insurance companies work. The UK life insurance suicide clause is still a thing, but insurers are much more understanding when it comes to covering people with a history of mental health conditions.

A few years back, having depression or anxiety in your history often made life insurance hard to get or very costly. These days, with pressure from groups like the Financial Conduct Authority (FCA), insurers are taking a fairer approach. When you apply, they will ask about your mental health history, including:

- Your diagnosis (what your condition is).

- When you were diagnosed.

- Any time you spent in a hospital.

- The treatment you’re receiving (like talking therapy or medication).

Having a history of mental health issues will not automatically stop you from getting life insurance. If your condition is well-managed, you can often get a policy at a standard price. Insurers understand that a person who is looking after their mental health is a lower risk. The UK life insurance suicide clause is a protection against fraud, not a punishment for dealing with an illness.

Comparing UK Insurers and Their Suicide Clauses (2025)

To give you a proper idea of what’s what, let’s have a look at some of the big names in UK life insurance. This little table shows what you can expect from their policies in 2025, particularly their stance on the UK life insurance suicide clause, and what makes them tick.

| Insurer | Suicide Exclusion Period | Claim Payout Rate (2024/2025) | What People Say About Them |

| Legal & General | 12 months | 97.0% | A real household name. They’re known for being fair and reliable, with decent prices and a strong reputation for sorting things out when it counts. |

| Aviva | 12 months | 97.1% | You’ll see their name everywhere. They offer a huge range of products and are seen as one of the most financially secure companies out there. |

| Royal London | 12 months | 98.7% | They’re a mutual society, which is a bit different—it means they’re owned by their members, not shareholders. They have an outstanding payout rate and are generally considered a top choice. |

| Zurich | 12 months | 97.0% | Known for being a safe pair of hands. They’re excellent at handling trickier cases and offer robust protection that gives you serious peace of mind. |

| Vitality | 12 months | 91.9% | They stand out from the crowd. Their unique ‘Vitality Programme’ rewards you for being healthy with all sorts of discounts and perks, which can be a real bonus. |

Just a quick note: Payout rates can change a little bit each year, and they cover all claims, not just suicide. The UK life insurance suicide clause is pretty much the same across the board, with most using that 12-month period. Always have a read of your specific policy’s terms and conditions before you sign on the dotted line.

The Good, the Bad, and the Plain Reality of the UK Life Insurance Suicide Clause

The UK life insurance suicide clause is a bit of a tricky thing. It’s a simple rule on paper, but it has some big consequences. Let’s weigh up the good and bad bits.

The Good Bits:

- It’s a Safety Net Against Fraud: This is the most important part. It’s the number one way to stop people from taking out a policy with the immediate, devastating intention of self-harm just to get a payout. Without it, the whole insurance system would collapse, and no one could get cover.

- It Keeps Premiums Sensible: By stopping that sort of fraud, the UK life insurance suicide clause helps keep the cost of life insurance down for everyone. It makes sure that life insurance stays a workable solution for normal families.

- A Small Act of Kindness: Even if the worst happens within the exclusion period, the clause makes sure the family gets back all the money that was paid in. It’s not a lot, but it’s something, and it shows a little compassion during an awful time.

The Not-So-Good Bits

- It Makes Things Harder: Losing someone close is already a storm to go through. On top of that, when the insurance money doesn’t come through, the family feels like the ground has been pulled out from under them. Instead of comfort, the clause often adds another layer of pain.

- It Feels Unfair Sometimes: The truth is, the rule doesn’t really see the difference between a long-term plan and a sudden mental health crisis. A person might have bought the policy with every good intention, never even thinking about self-harm, yet their family is left with nothing. That can feel harsh and unfair.

- Most People Don’t Even Know About It: Many families assume life insurance covers everything from day one. They only discover the suicide clause when they are already dealing with a loss. And honestly, that shock can be as painful as the financial loss itself.

- At the end of the day, the UK life insurance suicide clause has two sides. It may help protect the system, but for families, it can turn an already terrible time into something even heavier.

Understanding the UK life insurance suicide clause is about seeing its purpose in the bigger picture of the insurance world, while also appreciating the huge emotional toll it can take on families who are already struggling.

Your 2025 UK Life Insurance Checklist

In 2025, the legal side of life insurance in the UK is still pretty much the same. A payout is generally not subject to Income Tax or Capital Gains Tax. However, the money can be counted as part of your estate when it comes to Inheritance Tax (IHT). This is where you need to be smart.

To protect the payout from IHT, most people ‘write their policy in trust’. This simply means the money is held by special people (trustees) for your family, so it’s kept separate from your own estate. This one simple step can save your loved ones from a painful 40% tax bill and get the money to them much, much faster.

Top Tips from the Experts at primelifecover.com:

- Honesty is the Best Policy: When you fill out your application, you must be 100% truthful about your health and medical history. Lying or hiding information is called ‘non-disclosure’. If an insurer finds out you weren’t honest, they can deny a claim for any reason at all—not just for a death by suicide. It’s just not worth the risk.

- Pick the Right Policy: You can get a policy for a set number of years (term life) or one that covers you for your whole life (whole of life). The UK life insurance suicide clause applies to both. But on a whole of life policy, the exclusion period is such a tiny fraction of the total time you’re covered that it’s almost a non-issue.

- Give it a Health Check: Your life, health, and finances are always changing. Make it a habit to review your policy every year or so to make sure it still fits your family’s needs perfectly.

Your Questions Answered about the UK Life Insurance Suicide Clause

1. Does the suicide clause reset if I get a new policy?

Yes, this is a very important point. If you cancel an old policy and take out a brand-new one, the UK life insurance suicide clause will start all over again. So, if you had a policy for 10 years and then got a new one, you’d have to wait another 12 or 24 months for that clause to pass.

2. What about a death from an accidental overdose?

An accidental overdose would usually be covered by a life insurance policy, as it’s not a deliberate act of self-harm. However, if the overdose was intentional, it would fall under the UK life insurance suicide clause. The insurer would look at a coroner’s report to figure out the intent.

3. What if I just can’t afford my premiums anymore?

Whatever you do, don’t just stop paying! Call your insurer straight away. They might be able to help you out by letting you take a break from payments, or by reducing your cover to lower the monthly cost. Letting a policy lapse means the cover is gone, and so is any chance of a payout.

4. Can I get a policy with a history of mental health issues?

Absolutely. Having a history of mental health problems will not automatically stop you from getting life insurance. As we’ve mentioned, insurers are much more understanding these days and will look at how well your condition is managed. The UK life insurance suicide clause is a rule that applies to everyone’s policy, but it doesn’t mean you can’t get coverage in the first place.

5. Are there different rules in Scotland, Wales, or Northern Ireland?

No, the UK life insurance suicide clause and the laws around life insurance are standard across the entire United Kingdom.

The Final Word: Don’t Let Worry Stop You

Talking about the UK life insurance suicide clause is not easy, but it’s important to understand. The truth is, for most people this rule will never become a problem. It is mainly there to keep the system fair and safe, not to stop families from getting the cover they need.

What really matters is being honest when you fill out your application, reading your policy carefully, and making sure your family knows where the papers are and who they should contact. Life insurance is there to give peace of mind, and with the right knowledge, it can do exactly that.

If you feel ready to look for a policy that suits your needs, we can help.

[CTA: Compare UK Life Insurance Quotes Now!]

Disclaimer:

The information in this article is for general knowledge only and should not be seen as financial or legal advice. Policy terms and laws can change. Always read your policy document carefully and talk to a qualified financial advisor for advice that is specific to you

Author Box

Written by DN Patel

Founder & Life Insurance Specialist

Helping families in USA, UK, Canada & Australia choose the right life cover

📢 Stay connected for the latest insurance tips, updates, and guides!

👉 Follow us on Facebook